The clock showed 2:17 AM when I found myself staring at my laptop screen, frantically searching for business loan options. What started as a routine evening had turned into a financial emergency that couldn’t wait for traditional banking hours. Here’s the complete story of my midnight loan application journey and the lessons I learned along the way.

The 2 AM Crisis That Started It All

The Emergency That Couldn’t Wait Until Morning

Running a small manufacturing business means dealing with unexpected situations, but nothing prepared me for that Tuesday night crisis. Three different emergencies hit simultaneously, creating a perfect storm that demanded immediate action.

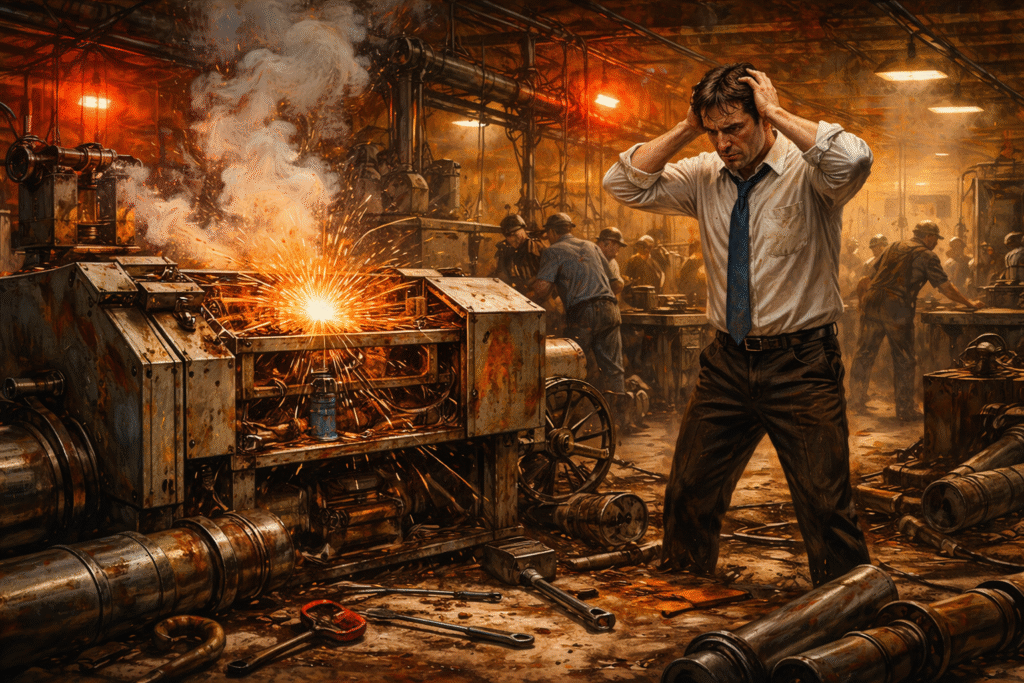

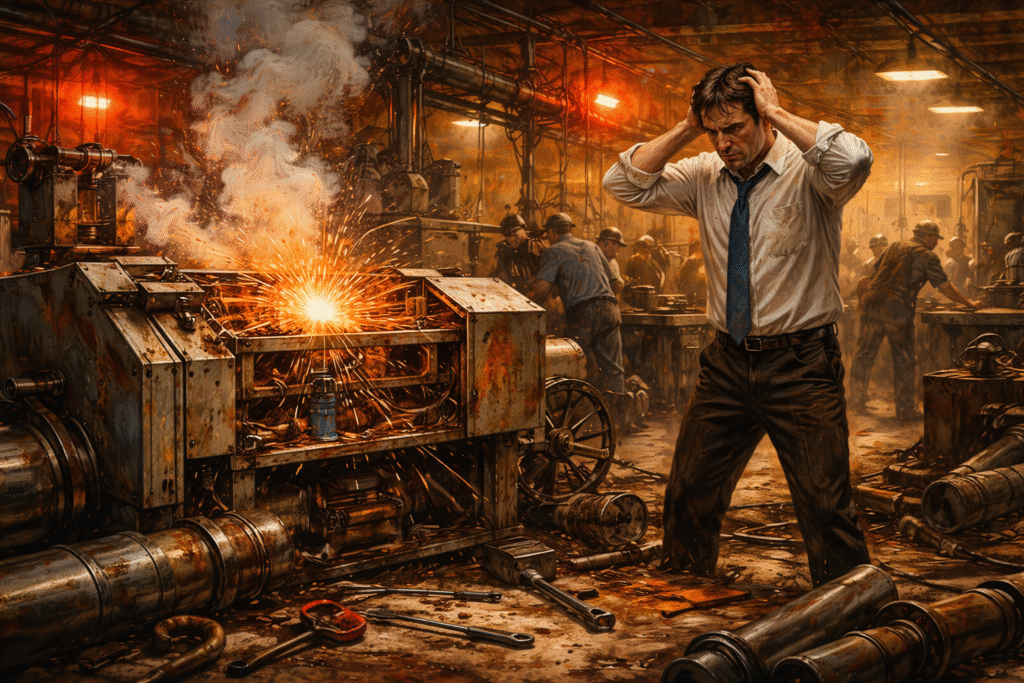

Equipment breakdown threatening next-day client deliveries

My primary packaging machine decided to give up at 9 PM, right after our evening shift ended. The repair technician quoted 3,30,200 for parts and emergency service, with work needed to start by 6 AM to meet our client commitments. Without those deliveries, I risked losing my biggest client and facing penalty fees that would exceed 30,000.

Cash flow gap between major client payment and immediate expenses

Like many small businesses, I was caught in the classic cash flow trap. A major client’s 15,00,000 payment was delayed by their accounting department until the following week, but my immediate expenses couldn’t wait. I had payroll due in two days, rent coming up, and now this equipment emergency.

Unexpected opportunity requiring immediate capital investment

To make matters more interesting, a supplier had contacted me earlier that day about a bulk inventory opportunity at 40% below normal prices. The catch? I needed to commit and pay by 10 AM the next day. This deal could save my business thousands over the next quarter, but only if I could secure the funds immediately.

Why Traditional Banking Wasn’t an Option

Bank branches closed and wouldn’t open for hours

At 2 AM on a Wednesday morning, my local bank wasn’t exactly taking calls. Even when they opened at 9 AM, I knew from experience that getting a loan officer’s attention would take days, not hours.

Previous experience with lengthy loan approval processes

Six months earlier, I had applied for a traditional business loan that took 45 days to process, required mountains of paperwork, and ultimately got rejected due to my business being “too new” despite solid revenue. I couldn’t afford to wait that long again.

Need for funds within 24-48 hours, not weeks

The equipment repair needed to start by dawn, and the inventory opportunity had a hard deadline. Traditional banking operates on different timelines than small business emergencies.

The Moment I Decided to Try Online Lending

Research into alternative funding options at midnight

I spent the first hour researching online lending platforms, reading about alternative financing options I’d heard other business owners mention. The promise of quick approvals and fast funding seemed too good to be true, but my options were limited.

Reading reviews and testimonials from other business owners

I dove deep into review sites, business forums, and testimonials. Some stories were encouraging – business owners getting approved within hours and receiving funds the next day. Others warned about high interest rates and aggressive repayment terms.

Weighing the pros and cons of instant loan platforms

The math was simple but sobering. Online lending would cost significantly more than traditional loans, but the alternative was potentially losing my biggest client and missing a major cost-saving opportunity. Sometimes expensive money is better than no money at all.

Navigating the Digital Application Maze

Choosing the Right Platform Among Dozens

Comparing interest rates and terms across multiple lenders

I opened tabs for eight different lending platforms, creating a spreadsheet to compare offers. Interest rates ranged from 18% to 65% APR, with terms varying from 3 months to 2 years. The variation was staggering and confusing.

Evaluating user interface and application complexity

Some platforms had clean, simple interfaces that walked me through the process step by step. Others felt like navigating a maze, with unclear requirements and confusing terminology. At 2 AM, user experience became surprisingly important.

Checking lender credentials and regulatory compliance

I spent time verifying each platform’s legitimacy, checking Better Business Bureau ratings, and looking up their regulatory compliance. Several platforms had concerning reviews about hidden fees and aggressive collection practices.

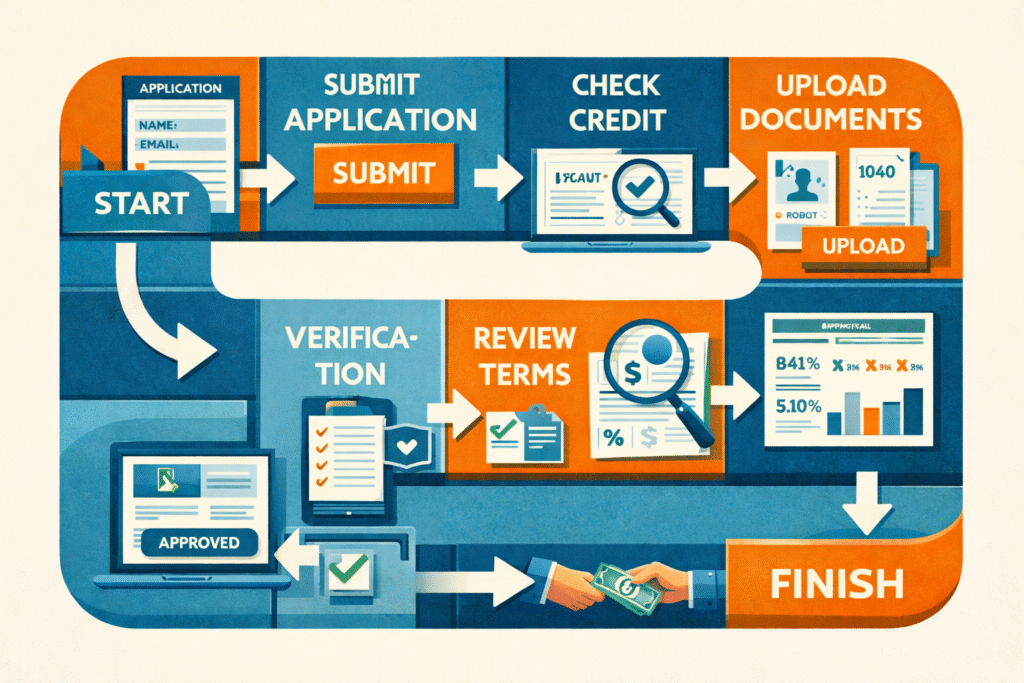

The Step-by-Step Application Process

Personal and business information requirements

Every platform wanted similar basic information: my SSN, business EIN, years in business, monthly revenue, and personal credit score. What surprised me was how much personal financial information they required, even for business loans.

Financial documentation and bank account linking

Most platforms used third-party services to connect directly to my business bank account, analyzing several months of transaction history automatically. This felt invasive but was certainly faster than uploading bank statements.

Identity verification and business validation steps

The verification process included uploading my driver’s license, business license, and recent utility bills. Some platforms used facial recognition technology to match my photos, which felt very modern but slightly unsettling at 2 AM.

Technical Challenges and User Experience Issues

Website crashes during peak hours

Two platforms crashed while I was mid-application, losing all my progress. Apparently, late-night and early-morning hours are peak times for emergency loan applications. Who knew so many other business owners were also up at 2 AM dealing with financial crises?

Document upload failures and format requirements

I encountered frustrating technical issues with document uploads. One platform only accepted PDFs under 2MB, another rejected my bank statements because they were “too recent” (apparently 1-day-old statements looked suspicious to their system).

Mobile app limitations versus desktop functionality

I tried switching to mobile apps when desktop sites became frustrating, but found the mobile experience even more limited. Complex financial applications really aren’t designed for smartphone screens.

The Waiting Game and What Happens Behind the Scenes

Instant Approval Claims vs. Reality

Understanding what “instant” actually means in lending

Despite marketing claims about “instant approval,” I learned that “instant” usually means “faster than traditional banks” rather than “immediate.” Most platforms provide preliminary approval within minutes, but final approval and funding take longer.

Automated decision systems and their limitations

The initial approval came from automated systems analyzing my bank account data and credit score. However, my application apparently triggered manual review requirements due to the late-night submission time and loan amount.

Cases requiring human review and additional documentation

My $10,000 loan request fell into a category requiring human underwriter review. This added 6-12 hours to the process, pushing my timeline from “instant” to “next business day” at best.

Algorithm-Based Decision Making Process

How AI evaluates creditworthiness in minutes

The automated systems analyzed my bank account transactions, looking for patterns in revenue, expenses, and cash flow. It was fascinating and slightly concerning to see my entire business reduced to algorithmic decision points.

Factors that influence automated approval or rejection

I learned that factors like application time (2 AM looked suspicious), recent bank overdrafts (I had one from two months ago), and even the device used for application could influence automated decisions.

The role of bank account analysis and transaction history

The platforms scrutinized every transaction, flagging large cash deposits, irregular income patterns, and business expenses that didn’t align with my stated business type. My coffee shop purchases apparently raised questions about my manufacturing business claims.

Communication and Updates During Review

Automated email and text message notifications

I received a steady stream of updates via email and text, though many were generic status messages that didn’t provide much useful information. The notifications did help manage my anxiety about the process.

Tracking systems and application status dashboards

Most platforms provided real-time dashboards showing application progress, but the stages were often vague: “Under Review,” “Processing,” “Final Approval Pending.” Not very helpful for planning purposes.

When and how lenders request additional information

Around 6 AM, I received requests for additional documentation: recent tax returns, explanation letters for irregular deposits, and updated bank statements. Each request added hours to the approval timeline.

The Approval, Terms, and Fine Print Reality Check

Understanding the True Cost of Speed

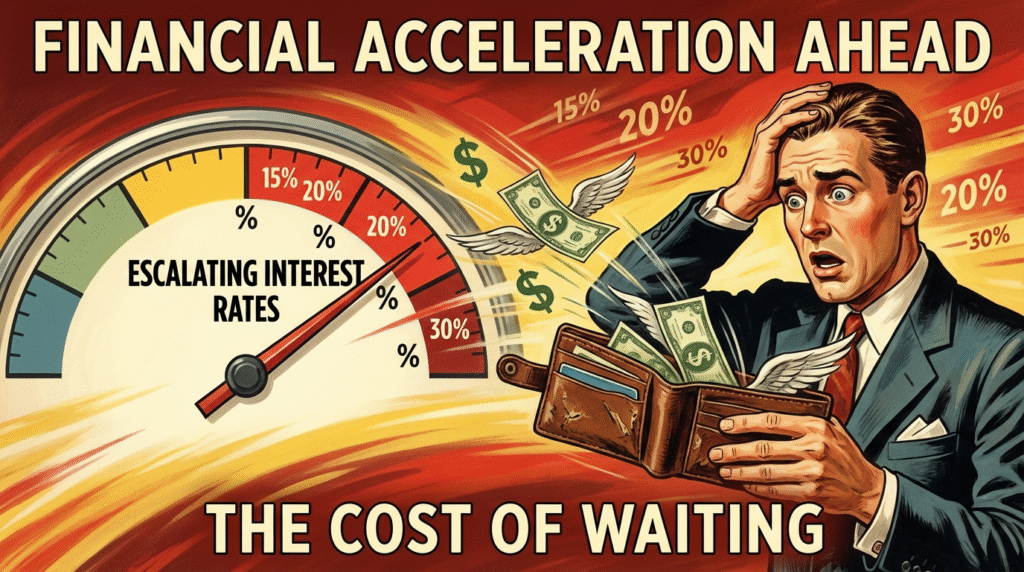

Interest rates compared to traditional business loans

My approved rate of 31% APR was shocking compared to traditional business loans (typically 6-15%), but made sense given the risk and speed factors. The cost of emergency funding became very real very quickly.

Hidden fees, origination charges, and early payment penalties

Beyond the interest rate, I discovered origination fees (3% of loan amount), processing fees ($150), and surprisingly, penalties for paying off the loan early. The total cost was significantly higher than the advertised rate.

Total cost of borrowing over the loan term

My $10,000 loan with a 6-month term would cost $13,200 total if paid as scheduled. That’s $3,200 in fees and interest for six months of financing. The math was sobering but necessary given my situation.

Loan Terms and Repayment Structure Analysis

Daily, weekly, or monthly payment options

I chose weekly payments of $507 over 26 weeks, rather than daily payments that would have been more expensive or monthly payments that carried higher interest rates. Weekly payments felt manageable for my cash flow patterns.

Impact of automatic withdrawals on business cash flow

Agreeing to automatic withdrawals reduced my interest rate by 1%, but meant giving the lender direct access to my business account every week. This required careful cash flow planning to avoid overdraft fees.

Consequences of missed payments and default terms

The default terms were aggressive: after 15 days late, they could accelerate the entire loan balance, charge additional fees, and begin collection activities. Missing payments wasn’t really an option.

Contract Details Most Borrowers Overlook

Personal guarantee requirements and implications

Despite being a “business loan,” I had to sign a personal guarantee, making me personally liable for the debt. My personal credit and assets were at risk if my business couldn’t repay.

Collateral or security interest in business assets

The lender secured the loan against my business equipment and inventory through a UCC filing. This meant they had legal claim to my assets if I defaulted.

Restrictions on business operations and additional borrowing

The agreement included restrictions on taking additional debt, selling major assets, or making significant operational changes without lender approval. These covenants felt restrictive but were standard.

The Money Arrives: What Actually Happens Next

From Approval to Funds in Your Account

Wire transfer timing and processing delays

Final approval came at 11 AM on Wednesday, but the wire transfer didn’t hit my account until 2 PM due to banking processing times. Even “instant” funding has logistical limitations.

Bank hold policies on large deposits

My bank placed a hold on part of the wire transfer, making only $5,000 immediately available. I had to call and explain the urgent situation to get the hold lifted for the remaining funds.

Verification requirements before accessing funds

Before releasing the full amount, my bank required verification that the wire transfer was legitimate business funding, not suspicious activity. This added another hour of phone calls and documentation.

Immediate Relief vs. Long-Term Impact

Solving the crisis that prompted the late-night application

The equipment repair was completed by Thursday morning, and I met my client deliveries. The inventory purchase went through, ultimately saving my business over $4,000 in the following quarter.

How quick access to capital affected business operations

Having immediate access to capital was genuinely business-saving in this instance. The ability to respond quickly to both the crisis and opportunity justified the high cost, at least in this specific situation.

Changes in daily cash flow management

The weekly loan payments forced me to implement better cash flow forecasting and management systems. Ironically, the expensive loan helped improve my financial discipline.

The Reality of Repayment Begins

First payment deduction and impact on business banking

The first automatic withdrawal of $507 hit exactly one week after funding. Seeing that money leave my account every week was a constant reminder of the true cost of emergency borrowing.

Adjusting business budgets for loan obligations

I had to restructure my business budget around the weekly payments, reducing discretionary spending and postponing some planned investments. The loan payments became a significant fixed expense.

Managing customer payments with automatic withdrawals

Coordinating customer payments with loan payment dates became crucial. I couldn’t afford to have the automatic withdrawal hit during a low cash flow period.

Lessons Learned and What I’d Do Differently

Mistakes Made in the Application Process

Not reading all terms and conditions thoroughly

At 2 AM under pressure, I skimmed through some of the fine print and missed several important details about fees and restrictions. Emergency situations don’t excuse poor due diligence.

Accepting the first approval instead of shopping around

In my urgency, I accepted the first reasonable approval rather than waiting to compare offers from multiple lenders. This probably cost me several hundred dollars in unnecessary fees.

Underestimating the true cost of emergency borrowing

I focused on getting the money quickly and didn’t fully calculate the total cost impact on my business until after signing. Emergency lending is expensive lending.

Better Alternatives and Preparation Strategies

Building business credit and relationships before emergencies

I should have established business credit lines and banking relationships during good times, not during crises. Preparation makes emergency funding both cheaper and easier to obtain.

Establishing business lines of credit for future needs

A business line of credit would have provided similar quick access to funds at much lower cost. These require advance planning but offer better emergency funding options.

Creating emergency funds and better cash flow management

Building a business emergency fund and improving cash flow forecasting would have reduced my need for expensive emergency lending. Prevention is cheaper than cure.

Advice for Other Business Owners Considering Instant Loans

When instant loans make sense versus other options

Instant loans make sense when the cost of not having immediate funds exceeds the high borrowing costs. They’re expensive solutions that sometimes provide necessary business value.

Red flags to watch for in online lending platforms

Be wary of platforms with unclear fee structures, aggressive sales tactics, extremely short repayment terms, or poor customer service reviews. Legitimate lenders are transparent about costs and terms.

Questions to ask before accepting loan terms

Always ask about total cost of borrowing, early payment options, fee structures, personal guarantees required, and what happens if you miss payments. Understanding the worst-case scenarios is crucial.

Summary

The world of instant business loans offers genuine solutions for urgent capital needs, but comes with significant costs and considerations. While technology has made accessing business funding faster than ever, the convenience of 2 AM applications shouldn’t overshadow careful evaluation of terms, costs, and long-term impact on your business. Success with instant lending requires understanding both the benefits and limitations of automated approval systems, while maintaining realistic expectations about timing, costs, and repayment obligations.

My midnight loan application ultimately saved my business relationships and created profitable opportunities, but the high cost served as an expensive lesson about the importance of financial preparation. The next time I face a business emergency, I’ll be better prepared with established credit lines, emergency funds, and stronger banking relationships.

Frequently Asked Questions

How quickly do instant business loans actually provide funds?

Most legitimate instant loan platforms provide funds within 1-3 business days after approval, despite “instant” marketing claims. Same-day funding is possible but rare and often comes with additional fees.

Are instant business loans more expensive than traditional bank loans?

Yes, significantly. Instant business loans typically carry interest rates 2-5 times higher than traditional bank loans, reflecting the higher risk and convenience factor of quick approval processes.

What credit score do I need for an instant business loan?

Most instant loan platforms accept credit scores as low as 500-550, but better rates and terms are available for scores above 650. Some platforms focus more on business cash flow than personal credit.

Can I pay off an instant business loan early without penalties?

This varies by lender. Many instant loan platforms allow early payoff without penalties, while others charge prepayment fees. Always check terms before accepting any loan offer.

What happens if I can’t make payments on an instant business loan?

Consequences include additional fees, damage to personal and business credit, potential legal action, and possible seizure of business assets if used as collateral. Most lenders will work with borrowers to modify payment plans before pursuing aggressive collection actions.